From ‘plan b’ to ‘plan v’: what the uk economy needs to reboot and rebalance growth

From ‘Plan B’ to ‘Plan V’: what the UK economy needs to reboot and rebalance growth

With the threat of stagflation and interest rate rises, the current

economic climate shows little sign of improvement in the near future. finds that the government’s severe austerity

programme, with its very pessimistic view of future UK growth is risking

the recovery through premature scrapping of our economic capital.

Policies such as the cap on skiled migrants and the planning

decentralisation wil reduce the potential for growth, not raise it. Instead,

the government should get the conditions right for increasing competition, innovation

and education, and focus on matching the UK’s comparative advantage with areas of

future growth such as higher education.

Britain, along with most of the developed world has been through the worst recessionsince the 1930s and more pain is set to come as the government’s austerityprogramme bites. With the economy contracting at the end of last year by 0.5 per centand Pfizer shutting down its main UK research lab (which created Viagra), theChancelor is looking for the economic equivalent of Pfizer’s little blue pil to boost theUK economy – a ‘Plan V’. How to get back to Growth: A Plan B to extreme austerity

The UK Government’s Plan A was a sharp acceleration in budget consolidation folowingits election in June 2010. Whereas Alistair Darling had committed to raising taxes andcutting spending by 5 per cent of GDP by 2016/17, Chancelor Osborne brought theplans forward by a year and increased the budget consolidation to 7 per cent of GDP:the toughest since the Second World War. He also “frontloaded” the consolidation somore pain is going to be borne this year than under Labour’s plans.

Austerity was necessary – the question is how much and how quickly. The acceleratedausterity of the present government endangers the recovery, but it also risks longerterm growth because of the premature scrapping of fixed capital and human capital. For example, many of those losing their jobs are becoming long-term unemployed whowil not recover their skils. Long term unemployment is particularly dangerous as theseindividuals give up searching for jobs and reduce pressure to keep wage inflation low.

In my opinion, the accelerated austerity programme is fundamentaly a mistake becauseit is grounded in an overly pessimistic view of the UK’s potential output. Just as therewas exaggerated optimism over the improvements of the supply side engendered byfinancial markets in the pre-crisis period, now there is excessive pessimism with someprophets of doom suggesting the UK has permanently lost 7 -10 per cent of itscapacity. This ignores real improvements in relative UK performance over the pastdecade and a half.

Unfortunately, this irrational anti-exuberance risks becoming a self-fulfiling prophecy:extreme austerity leads to premature capital scrapping which in turn fulfils theexpectation of lower growth.

But don’t we need this extreme austerity to reassure bond markets? We are in therealms of psychology, but I believe that the March 2010 budget contained a credible

deficit reduction programme. Britain’s debt is not enormous by historical standards (79per cent vs. a three century average of 118 per cent), it has a long maturity and wehave never had a formal default. The UK is not Greece. The advantage of frontloadingthe pain is more political than economic – voters’ memories are short, so in 4 years’time the pain wil hopefuly be forgotten. Reasons to be cheerful?

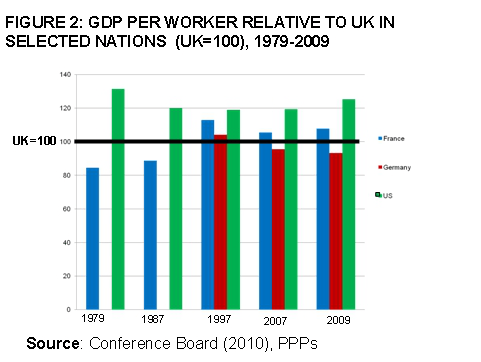

Despite al the doom and gloom about UK economic performance, the overal positionrelative to other countries has actualy been rather good. The UK had the fastestgrowth in per capita GDP of the six major advanced countries since 1997 (see Figure1), even including the savage downturn of the last few years. Part of this was due tolabour market policy supporting high employment rates. But an improvement also tookplace in productivity which has long been Britain’s Achiles heel (see Figure 2). Outputper worker overtook Germany’s and bridged some of the gap with France. Althoughthe gap did not close with the United States, the US has enjoyed a “productivitymiracle” since the mid 1990s, so just to keep hold of the tiger’s tail was quite anaccomplishment.

Human capital is one important factor which helped raise productivity, with theproportion of colege educated workers almost doubling since 1997 from 15 per centto 27 per cent. Tougher competition policy and an improved innovation performancealso played a part. Stil, a sizeable productivity gap remains whose roots lie in innovationand management. Mind the Productivity Gap

Britain has great strength in elite science, producing 14 per cent of the world’s topscientific papers with less than 1 per cent of the world’s population. Only the US doesbetter, and the UK surpasses the US considering scientific output per dolar ofuniversity funding. But commercializing these inventions to profitable ideas remains aproblem. Not only does the UK devote less of its national output to Research andDevelopment (R&D), this proportion declined from the late 1970s (see Figure 3) just asother nations were upping their R&D investments. This decline was halted and partialyreversed in the mid 2000s due to the introduction of a more generous tax and fundingregime for R&D and science.

It is a truism that the amount of spending on “hard” technologies is less important than

how these investments are used. After al, new technologies are available the worldover, but why do some countries and firms appear to make much better use of themthan others?

The man on the street’s answer is easy: “It’s management, stupid”. Economists havebeen traditionaly sceptical of this explanation, however, in large part because it is sot

this. It turns out that the common sense answer was right al along: management realymatters!

The UK is distinctly mid-table in the management league. The US leads the pack andthere is a “Premier League” of Japan, Germany and Sweden. Emerging countries likeIndia and China are unsurprisingly at the bottom, but they are not too far behindSouthern European nations such as Greece and Portugal.

Although the cross country averages are eye-catching, there is huge variation ofmanagement within every country. Three factors turn out to be major drags onmanagement quality: low competition, human capital and primogeniture (i.e. selectingthe CEO as the eldest son of the firm’s founder). These three factors account foressentialy al the gap in management between the UK and the US. How to foster long-term growth: Plan V

What should a growth strategy look like? It must have three elements: modesty,prescience and realism. Modesty means admitting that we don’t know exactly wheregrowth wil come from. But what we need is to get the conditions right in the countryso that ideas flourish and firms can easily grow to exploit these opportunities. Prescience means a rough and ready mapping out future growth sectors and realismmeans deciding where our comparative advantages lies (both current and nascent).

1. Competition – Trade policies (such as reinvigorating the Doha Round) and a more

flexible planning regime would be important policy wins here, as wouldstrengthening market discipline in the public sector. The problem of publicspending is not the level, but how it is spent. Evidence from hospitals, forexample, shows that increased competition between trusts helps improvemanagement and save patient lives.

2. Taxation – The level of taxation is less important than simplicity, stability and

absence of distortions. As an example, we could abolish the 100 per cent relief oninheritance tax for business assets within family firms. This distortion encourages

family firms which reduce productivity through poor management.

3. Human Capital – The UK does wel at the top end of the skils distribution with big

increases in graduates, but very badly at the bottom end with large proportions ofinnumeracy and iliteracy. Reforms to underachieving schools, strengtheningapprenticeships and maintaining support for low income families to stay at school(e.g.) are necessary

4. Financial Markets – The catalyst for the Great Recession was the implosion in the

financial sector. A major issue here is dealing with the problem of many banksbeing This requires a mixture of regulation and reducing the sizeof institutions carrying systemic risk.

5. Innovation – Ideas are promiscuous: they benefit the imitators more than the

original inventors, so the market wil under-provide investment in innovation. Thesocial returns to R&D for example, are about as private returns. Doing more R&D helps a country like the UK catch up with leading nations boththrough imitation, but also through a faster diffusion of knowledge. You needsome to know what the breakthroughs are at the frontier ofknowledge. This means generous support to basic science and also maintainingand strengthening the current system of R&D tax credits. By contrast, the plan tointroduce a “patent box” to subsidise existing intelectual property is a waste ofmoney as it wil do nothing to encourage R&D. The £1 bilion a year cost of thepatent box could be better spent on other innovation incentives.

Guessing future growth sectors seems like a fool’s errand. But we do have some ideasof where these are – for example, healthcare, education, green technologies, businessservices and digital businesses. Similarly the UK has clear comparative advantages inareas such as bio-pharmaceuticals, financial and business services, creative industriesand some areas of ICT (e.g. Autonomy and ARM). So the task is not hopeless – it ishard to be precise, but there are examples, such as higher education.

Higher Education is a sector where the UK has some comparative advantage withglobaly recognised universities that attract the second largest proportion of overseasstudents in the world. In order to create a better higher education market, the increasein the fees cap and the reduction in direct subsidy are the right direction of travel, eventhough the speed and uncertainty are creating severe problems. More damaging,however, is the decision to cap net immigration at 100,000 per year, as wel as the cutin “tier 1” visas for the exceptionaly talented and the threat to the Post Study WorkVisa. This is economic suicide, and the government should be doing the exact opposite– making it much easier for the very talented to come to the UK to work and study. Thiswil boost a major sector, increase innovation and productivity and may even help curtailinequality by providing more competition for the highly educated.

There is a lot to be optimistic about: the UK made progress in bridging the productivitygap since 1997. But if we remain excessively pessimistic about our potential capacity,we wil continue down the current path of severe austerity. The end of this journey wilindeed be anemic growth and poor employment prospects for years to come. It’s timefor a Plan V.

On 17 February, John Van Reenen spoke at the LSE event, Where is Future GrowthGoing to Come From?to download a podcast of the event (40 mb, MP3)

E.C.Safety Data Sheets Tradename: mega-Model Resin (Rapid hardening medelation resin /Powder) 1. Identification of the substance/preparation and of the company/undertaking Information on the product Trade name: mega Model Resin Powder Use / Purpose : Cold-curing acrylic, powder component of the 2-component acrylic system (polymer & monomer) for the purpose o

human C-reactive protein Instant ELISA BMS288INST Enzyme-linked immunosorbent assay for quantitative Not for diagnostic or therapeutic procedures. human C-reactive protein BMS288INST TABLE OF CONTENTS 1 Intended Use The human C-reactive protein Instant ELISA is an enzyme-linked immunosorbent assay for the quantitative detection of human C-reactive protein leve

From ‘Plan B’ to ‘Plan V’: what the UK economy

From ‘Plan B’ to ‘Plan V’: what the UK economy

deficit reduction programme. Britain’s debt is not enormous by historical standards (79per cent vs. a three century average of 118 per cent), it has a long maturity and wehave never had a formal default. The UK is not Greece. The advantage of frontloadingthe pain is more political than economic – voters’ memories are short, so in 4 years’time the pain wil hopefuly be forgotten.

deficit reduction programme. Britain’s debt is not enormous by historical standards (79per cent vs. a three century average of 118 per cent), it has a long maturity and wehave never had a formal default. The UK is not Greece. The advantage of frontloadingthe pain is more political than economic – voters’ memories are short, so in 4 years’time the pain wil hopefuly be forgotten.

Human capital is one important factor which helped raise productivity, with theproportion of colege educated workers almost doubling since 1997 from 15 per centto 27 per cent. Tougher competition policy and an improved innovation performancealso played a part. Stil, a sizeable productivity gap remains whose roots lie in innovationand management.

Human capital is one important factor which helped raise productivity, with theproportion of colege educated workers almost doubling since 1997 from 15 per centto 27 per cent. Tougher competition policy and an improved innovation performancealso played a part. Stil, a sizeable productivity gap remains whose roots lie in innovationand management. this. It turns out that the common sense answer was right al along: management realymatters!

The UK is distinctly mid-table in the management league. The US leads the pack andthere is a “Premier League” of Japan, Germany and Sweden. Emerging countries likeIndia and China are unsurprisingly at the bottom, but they are not too far behindSouthern European nations such as Greece and Portugal.

this. It turns out that the common sense answer was right al along: management realymatters!

The UK is distinctly mid-table in the management league. The US leads the pack andthere is a “Premier League” of Japan, Germany and Sweden. Emerging countries likeIndia and China are unsurprisingly at the bottom, but they are not too far behindSouthern European nations such as Greece and Portugal.